All Categories

Featured

Table of Contents

Inherited annuities come with a fatality benefit, which can give financial safety and security for your loved ones in the occasion of your fatality. If you are the recipient of an annuity, there are a few guidelines you will certainly require to follow to acquire the account.

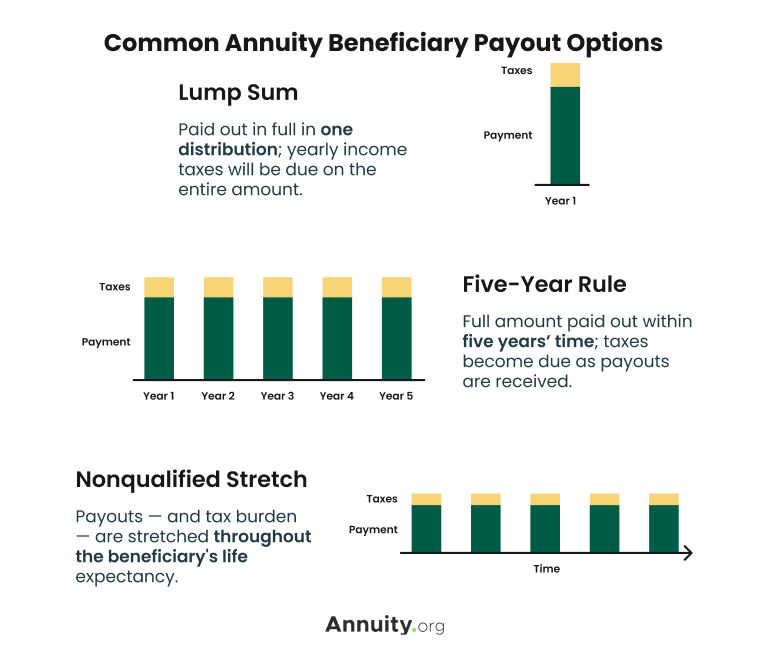

Third, you will certainly need to offer the insurance provider with various other called for paperwork, such as a duplicate of the will or count on. Fourth, relying on the kind of inherited annuity and your personal tax scenario, you may require to pay tax obligations. When you acquire an annuity, you have to pick a payout option.

With an immediate payment choice, you will begin getting repayments as soon as possible. Nevertheless, the settlements will be smaller than they would certainly be with a delayed option because they will be based upon the current value of the annuity. With a deferred payout option, you will certainly not start receiving repayments later.

When you inherit an annuity, the tax of the account will depend on the kind of annuity and the payout choice you pick. If you acquire a typical annuity, the payments you get will be strained as ordinary income. If you inherit a Roth annuity, the payments you get will not be tired.

Is there tax on inherited Annuity Income

If you select a deferred payment option, you will certainly not be tired on the growth of the annuity until you start taking withdrawals. Consulting with a tax obligation consultant before acquiring an annuity is very important to guarantee you comprehend the tax effects. An acquired annuity can be a fantastic means to provide economic safety and security for your liked ones.

You will certainly additionally need to follow the regulations for inheriting an annuity and pick the best payment option to suit your requirements. Be sure to talk with a tax obligation expert to guarantee you recognize the tax obligation implications of inheriting an annuity - Annuity cash value. An acquired annuity is an annuity that is given to a recipient upon the death of the annuitant

To inherit an annuity, you will certainly require to offer the insurance coverage firm with a duplicate of the death certification for the annuitant and complete a recipient type. You might need to pay taxes depending upon the kind of inherited annuity and your individual tax obligation circumstance. There are 2 main types of inherited annuities: standard and Roth.

The taxes of an inherited annuity will certainly rely on its kind and the payment choice you choose. If you inherit a conventional annuity, the payments you obtain will be taxed as average income. If you acquire a Roth annuity, the payments you receive will certainly not be exhausted. If you select a prompt payment option, you will certainly be exhausted on the annuity's development as much as the day of inheritance.

Do beneficiaries pay taxes on inherited Deferred Annuities

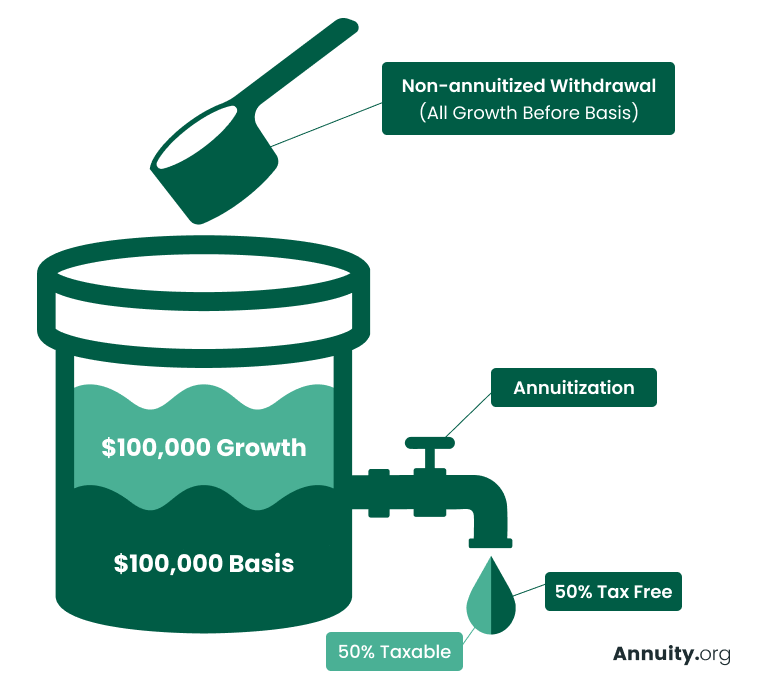

Just how an acquired annuity is exhausted depends on a range of elements, however one trick is whether the cash that's appearing of the annuity has actually been taxed before (unless it remains in a Roth account). If the cash dispersed from an annuity has not been taxed in the past, it will undergo tax.

In enhancement to owing revenue taxes, you may be struck with the internet financial investment revenue tax obligation of 3.8 percent on circulations of earnings, if you exceed the yearly thresholds for that tax obligation. Acquired annuities inside an individual retirement account also have special circulation rules and enforce other requirements on heirs, so it is very important to comprehend those policies if you do inherit an annuity in an IRA. A certified annuity is one where the owner paid no tax on payments, and it might be kept in a tax-advantaged account such as typical 401(k), standard 403(b) or typical IRA. Each of these accounts is moneyed with pre-tax cash, implying that taxes have actually not been paid on it. Considering that these accounts are pre-tax accounts and revenue tax obligation has actually not been paid on any of the money neither contributions neither revenues distributions will undergo regular earnings tax obligation.

A nonqualified annuity is one that's been bought with after-tax cash, and distributions of any payment are not subject to earnings tax due to the fact that tax has currently been paid on contributions. Nonqualified annuities consist of two major types, with the tax therapy relying on the kind: This sort of annuity is bought with after-tax cash in a routine account.

Any type of normal distribution from these accounts is free of tax on both added cash and revenues. At the end of the year the annuity company will submit a Form 1099-R that reveals precisely how a lot, if any kind of, of that tax year's distribution is taxed.

Beyond income tax obligations, an heir might likewise need to calculate estate and estate tax. Whether an annuity undergoes revenue tax obligations is an entirely separate matter from whether the estate owes inheritance tax on its worth or whether the heir owes estate tax on an annuity. Estate tax obligation is a tax assessed on the estate itself.

The rates are dynamic and variety from 18 percent to 40 percent. Individual states might likewise impose an inheritance tax on money distributed from an estate. In contrast, inheritance tax obligations are taxes on a person who obtains an inheritance. They're not analyzed on the estate itself however on the beneficiary when the properties are gotten.

Taxes on Variable Annuities inheritance

government does not evaluate estate tax, though 6 states do. Fees array as high as 18 percent, though whether the inheritance is taxable depends upon its dimension and your partnership to the giver. Those inheriting large annuities should pay attention to whether they're subject to estate tax obligations and inheritance tax obligations, beyond just the typical income tax obligations.

Beneficiaries ought to take notice of potential inheritance and inheritance tax, also.

It's a contract where the annuitant pays a lump amount or a series of premiums in exchange for a guaranteed earnings stream in the future. What occurs to an annuity after the proprietor passes away pivots on the certain information outlined in the contract.

Various other annuities provide a death advantage. This attribute allows the owner to mark a beneficiary, like a spouse or child, to get the remaining funds. The payment can take the form of either the entire continuing to be equilibrium in the annuity or an ensured minimum amount, typically whichever is higher.

It will plainly determine the beneficiary and possibly lay out the available payout options for the survivor benefit. Having this information helpful can assist you browse the procedure of receiving your inheritance. An annuity's fatality advantage guarantees a payout to a designated beneficiary after the proprietor passes away. The specifics of this advantage can differ depending on the type of annuity, when the owner passed away and any type of optional cyclists contributed to the agreement.

{kind=link}

Table of Contents

Latest Posts

Exploring Fixed Indexed Annuity Vs Market-variable Annuity Key Insights on Your Financial Future What Is Immediate Fixed Annuity Vs Variable Annuity? Benefits of What Is A Variable Annuity Vs A Fixed

Understanding Financial Strategies Everything You Need to Know About Financial Strategies What Is Fixed Annuity Or Variable Annuity? Advantages and Disadvantages of Choosing Between Fixed Annuity And

Decoding What Is A Variable Annuity Vs A Fixed Annuity Everything You Need to Know About Financial Strategies What Is the Best Retirement Option? Advantages and Disadvantages of Choosing Between Fixed

More

Latest Posts